Wine prices vs. inflation

Why it’s cheaper to drink wine today than 10 years ago

At a time when inflation dominates everyday life - from food and energy to housing and services - wine has a surprising position in the global economy. Despite higher shelf prices, wine has actually become cheaper to drink - at least in real terms. Adjusted for inflation, the purchasing power required to buy an average bottle of wine today is lower than it was a decade ago.

Understanding this apparent contradiction requires distinguishing between nominal prices and real prices.

Nominal prices have risen — but inflation has risen faster

Wine prices have increased in nominal terms over the past decade. Export prices, retail prices, and producer costs are all higher today than they were ten years ago. However, global headline inflation has risen even more sharply.

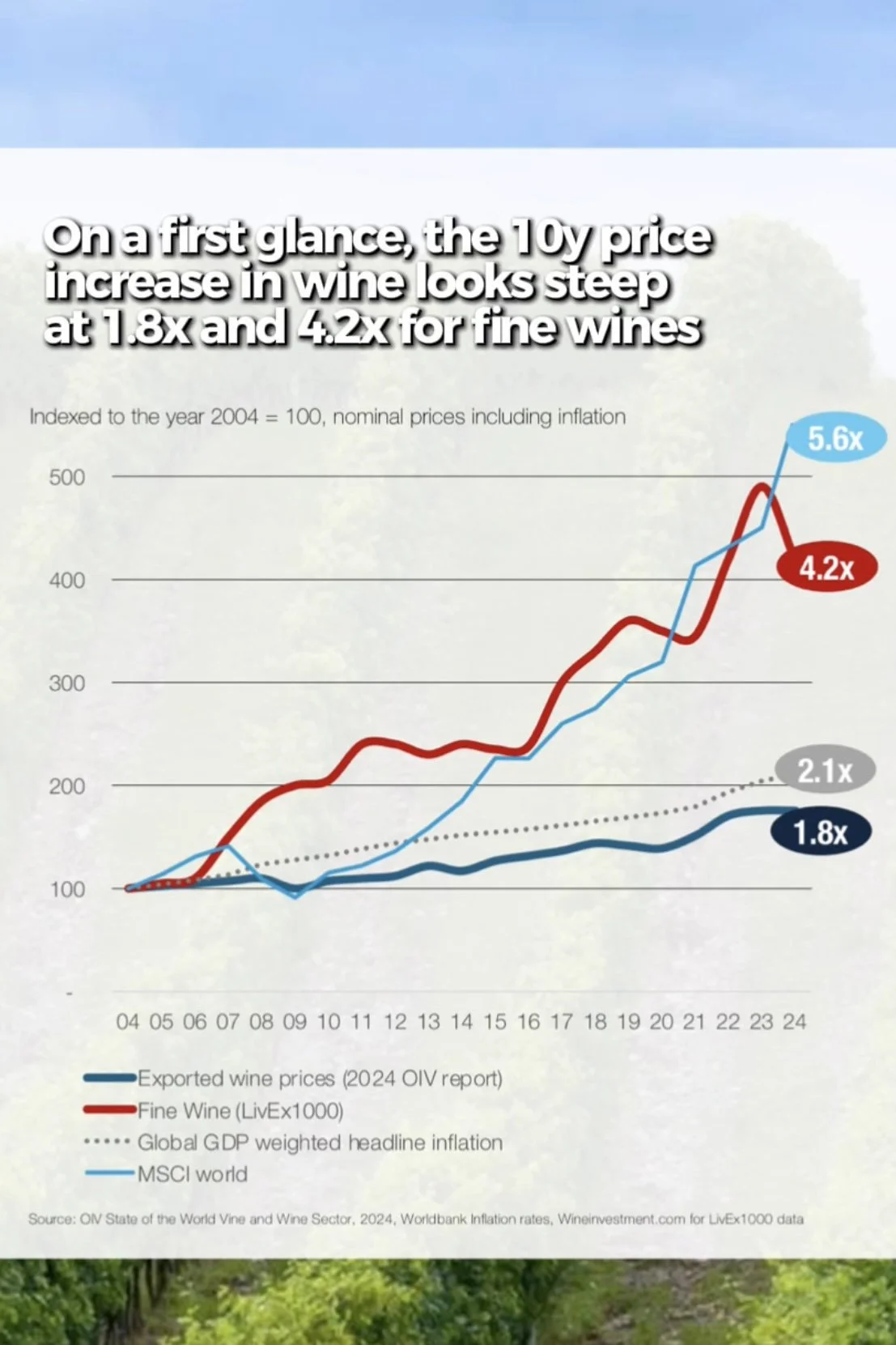

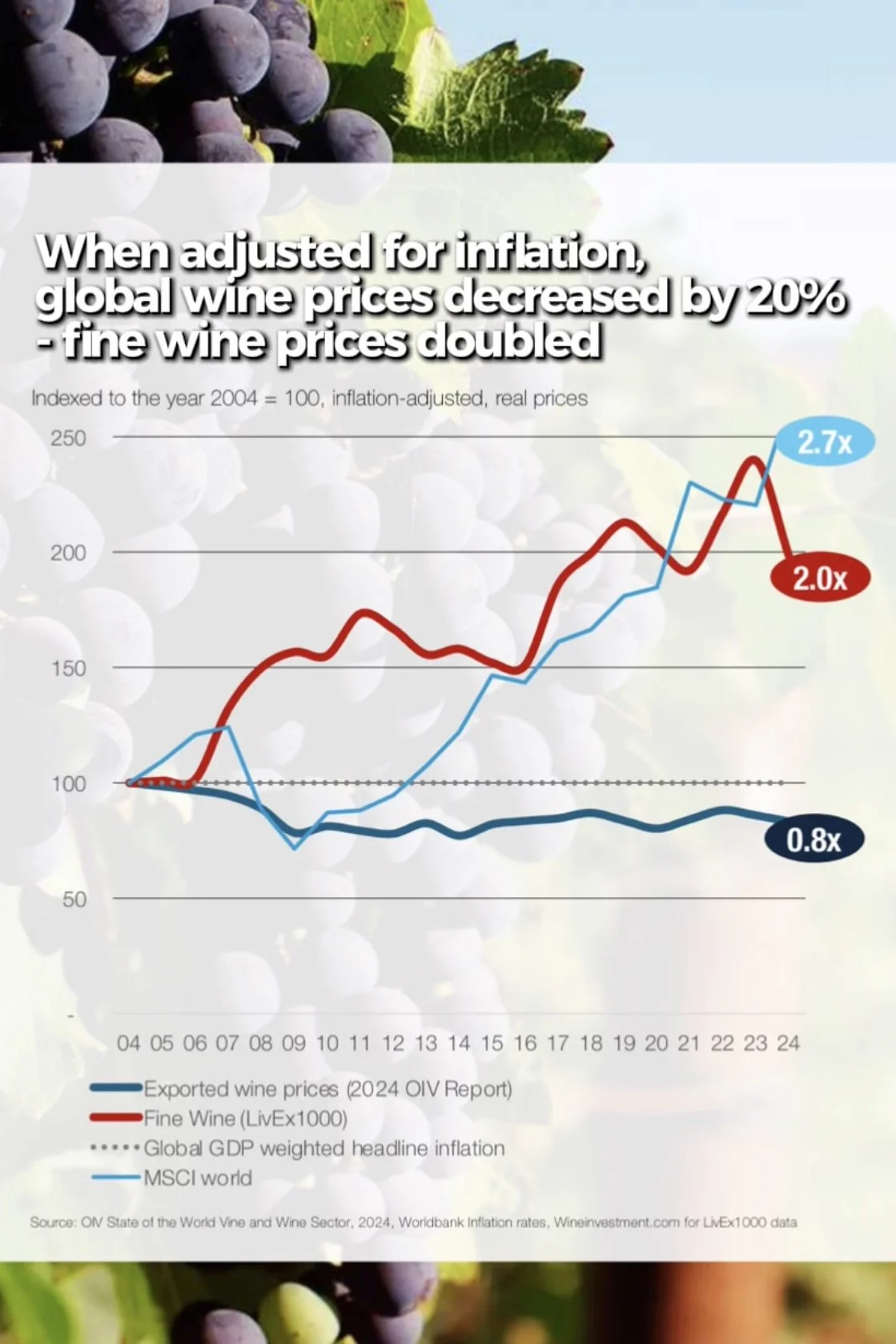

When prices are indexed to 2004, global wine export prices have increased by roughly 1.8×, while global inflation has risen by around 2.1×. The result: a steady decline in real wine prices. In practical terms, wine absorbs a smaller share of household income today than it did a decade ago - a rare outcome in an inflationary environment.

Why wine defies inflation

This divergence between wine prices and inflation is not accidental. Several structural forces have kept sustained downward pressure on wine prices in real terms.

Global oversupply remains the dominant factor. Wine production has expanded in many regions, while consumption has stagnated or declined in traditional wine-drinking markets. Excess supply has limited producers’ ability to pass rising costs on to consumers.

Intense global competition reinforces this dynamic. Wine is a highly tradable product with thousands of substitutable alternatives across price points and regions. Retailers and importers have resisted price increases, often forcing producers to absorb higher costs.

Productivity gains have also played a role. Mechanisation, improved vineyard management, and advances in logistics have offset increases in labour, energy, and packaging costs, further suppressing real price growth.

Fine wine is the exception

While everyday wine has become cheaper in real terms, fine wine has followed a very different path.

Prices for investment-grade wines tracked by Liv-ex indices have risen substantially faster than inflation. Indexed to 2004, fine wine prices have increased by approximately 4.2× in nominal terms and around 2.0× in real terms. This means that fine wine has not only preserved purchasing power, but meaningfully increased its real value over the long run.

This divergence highlights a growing polarisation in the wine market:

Mass-market and premium-everyday wines struggle to keep pace with inflation

Scarce, collectible wines behave more like luxury assets, driven by rarity, ageing potential, and global wealth effects

Fine wine vs. global equities: what kind of asset is wine?

Comparing fine wine with global equities, represented by the MSCI World Index, helps clarify what fine wine is - and what it is not - as an asset class.

Since 2004, global equities have outperformed fine wine in absolute terms. The MSCI World has risen by roughly 5.6× in nominal terms and about 2.7× in real terms, compared with 4.2× nominal and 2.0× real for fine wine.

However, fine wine is not designed to compete with equities on headline returns.

Equities derive value from earnings growth, reinvestment, and productivity gains. In a long-term perspective, they are also inflation hedged, as price increases are passed through.

Fine wine in turn is a real asset, shaped by scarcity, cultural demand, and time-dependent consumption. Every bottle consumed permanently reduces supply, creating a structural scarcity dynamic absent from financial assets.

A different risk profile

Fine wine has historically exhibited:

Lower long-term volatility than equities

Shallower drawdowns during equity market crises

Low correlation with traditional financial assets

These characteristics make fine wine less suitable as a return-maximising investment, but attractive as a diversifying asset within a broader portfolio.

Unlike equities, fine wine generates no cash flows or dividends. Its value lies in capital preservation, optionality, and the asymmetric upside created by scarcity and global demand - with the unique feature that the asset can ultimately be consumed.

Cheaper to drink, harder to produce

For consumers, the implication is clear: wine offers much better value today relative to ten years ago. For producers, the picture is more challenging. Rising input costs combined with weak real price growth are compressing margins and accelerating structural change across the industry.

In short, while wine may feel more expensive at the till, inflation tells a different story. Adjusted for purchasing power, it is cheaper to drink wine today than it was ten years ago — while fine wine has quietly established itself as a distinct real-asset class that preserves value rather than chasing market-beating returns.